The payments landscape just got more demanding. With Visa's Acquirer Monitoring Program (VAMP) now in full enforcement and merchant excessive thresholds dropping from 2.2% to 1.5% in April 2026, understanding your fraud metrics isn't optional anymore, it's survival.

But here's the thing most merchants miss: VAMP compliance isn't just about avoiding penalties. Done right, it becomes your competitive advantage.

What actually changed with VAMP?

Visa launched VAMP on April 1, 2025, consolidating the former Visa Dispute Monitoring Program (VDMP) and Visa Fraud Monitoring Program (VFMP) into a single framework with stricter thresholds. After a six-month warning period, enforcement began on October 1, 2025.

The shift is fundamental. Rather than treating disputes as an unavoidable cost of doing business, VAMP incentivizes merchants to investigate root causes, tighten fraud prevention controls, and maintain clean transaction records. Merchants who sustain low chargeback and fraud rates benefit from improved authorization rates, as issuers are more likely to approve transactions from sellers with a proven track record of low-risk activity.

Over time, this strengthens the merchant's relationship with issuing banks, which develop greater confidence in the legitimacy and quality of the merchant's transaction flow.

The metrics that matter

VAMP evaluates fraud activity using standardized performance thresholds based on three core metrics:

- TC40 Fraud Reports: These include fraud notifications reported by issuing banks, typically linked to unauthorized or fraudulent transactions.

- TC15 Disputes: This reflects the total chargeback count, including cases resolved through Rapid Dispute Resolution (RDR). Since RDR transactions are handled before becoming formal disputes but may still appear in TC40 reports, they should be excluded from the TC15 calculation to avoid double counting.

- TC05 CNP Settled Transactions: This represents the total number of card-not-present transactions that have been successfully settled, serving as the baseline for calculating your VAMP ratio.

The formula is straightforward:

VAMP Ratio = (TC40 Fraud Reports + TC15 Disputes - RDR hits) / TC05 CNP Settled Transactions

The hidden complexity of TC40 data

Here's where it gets tricky. TC40 data isn't straightforward, and interpreting it correctly requires understanding several complicating factors:

Processor Differences: Depending on your payment processor, the same fraudulent event may be linked to a successful sale, a failed authorization, or even a refunded transaction. Because of these differences, the numerator and denominator in fraud calculations can vary between systems.

Deduplication Logic: Visa applies internal deduplication rules to TC40 reports, but merchants and acquirers rarely know exactly how these rules work. The same transaction may appear under multiple fraud classifications, identical transactions may be reported in different months, or fraud records may reference different transaction identifiers.

In real-world reporting, you might see a single transaction flagged multiple times with different fraud classifications. This makes manual reconciliation extremely difficult.

What can actually be disputed? In practice, declined transactions represent the clearest case for disputes with Visa. If fraud reporting references transactions that were never successfully authorized, merchants may have grounds to challenge the record. However, this process often requires coordination with acquirers and processors.

The refund myth that's costing you

Many merchants believe that issuing refunds or using dispute prevention tools automatically reduces fraud metrics. That assumption is incorrect.

1. Refunding a transaction removes it from fraud: It doesn't. Issuing a refund resolves the customer issue, but it does not cancel the TC40 record. Refunded transactions may still appear in TC40 reports, TC40 entries may reference the refund transaction ID directly, and your fraud rate remains unaffected by refund activity.

2. RDR prevents chargebacks, so it improves my fraud rate: RDR improves dispute metrics only. It has no impact on TC40 fraud records whatsoever. It does not remove or reduce TC40 fraud records. Relying on RDR alone creates a false sense of compliance security.

Turning metrics into action

Effective VAMP compliance begins with building a measurement infrastructure that goes beyond surface-level reporting and drives real operational action. Many merchants unknowingly underestimate their fraud exposure by falling into common analytical traps:

- Assuming refunds remove fraud records

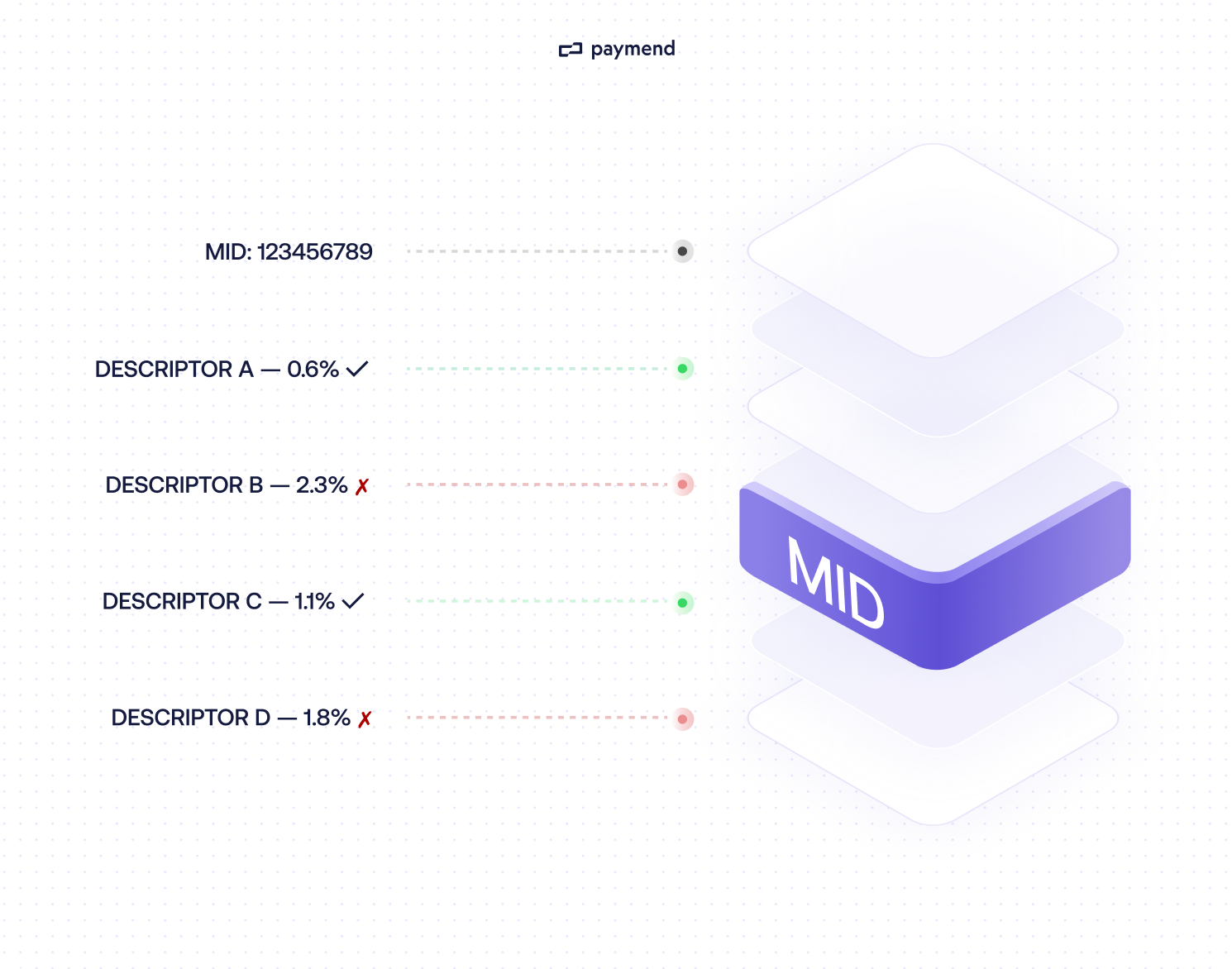

- Ignoring descriptor-level monitoring

- Analyzing only MID-level metrics

- Relying exclusively on chargeback prevention tools

- Failing to reconcile TC40 data against processor records

These blind spots delay detection and allow risk to compound silently beneath the threshold of visibility. Measurement only becomes valuable when it triggers operational response.

Strong VAMP monitoring programs include:

- Regular fraud rate tracking

- BIN & geography analysis

- Descriptor-level analysis

- TC40 anomaly detection

- Early escalation protocols

To build an effective monitoring framework and put this into practice, merchants should:

- Establish internal fraud rate dashboards using TC40 data

- Track metrics by descriptor, BIN, geography and product line

- Reconcile processor transaction data with fraud reporting

- Implement early-warning thresholds before official limits

- Audit fraud prevention tools beyond basic chargeback protection

The ultimate goal is not simply to measure fraud, but to understand its structure, who is generating it, where it originates, and how it behaves, so that every metric becomes a prompt for targeted, timely action.

How Paymend handles VAMP complexity

At Paymend, we assume full payment liability on behalf of the businesses we serve. That means fraud exposure, chargeback risk, and VAMP compliance for the transactions we process are our responsibility.

Thanks to our expertise in TC40 data and the mechanics of chargeback and fraud reporting, we help businesses dispute illegitimate chargebacks effectively, recover lost revenue, and keep their chargeback ratio within Visa's acceptable thresholds. Our analytics capabilities flag suspicious transactions before they escalate into formal disputes, reducing fraud rates proactively.

With Paymend:

- Reduced chargeback ratios

- Proactive fraud prevention

- Real-time performance monitoring

- Stronger issuer relationships

- Higher authorization rates

Staying off Visa's radar starts with knowing where you stand. At Paymend, we handle the complexity so you can focus on growing. Download the full guide here!