When you outgrow a single-PSP setup, payment performance becomes an ops problem. Issues like routing rules and retry logic can quietly cap your approval rate. That matters because issuers remain conservative in card-not-present transactions.

Nearly half of merchants estimate that up to 5% of legitimate orders are incorrectly declined as fraud, equating to around $50 billion in lost revenue across the e-commerce industry.

The next step is to see what a payment management system could do for your business, and we’re shortlisting the best picks for 2026 so you don’t have to.

What are payment management systems?

A payment management system is the control layer that decides how card payment authorization attempts are routed, retried, and reported across your stack. It’s the system of record for payment logic, including:

- Which PSP or acquirer gets the attempt

- What happens on a soft decline

- How tokens and payment methods are handled across providers

- How finance gets clean reporting

Scaled merchants adopt these systems to fix problems with fragmented visibility, such as performance scattered across providers, and brittle decision-making caused by a lack of centralization across payment gateway settings.

The commercial goal of using a payment management system is to stabilize payment performance (including approval rate outcomes) and clean up reconciliation. These tools can help you achieve fewer payments-related problems without rebuilding your stack every time you add a provider or expand globally.

Finance, operations teams, and payments and product owners are the primary users of these systems. You’ll typically need a payment management system once you’re running ops like higher volume and multiple PSPs or acquirers. You probably don’t need one if you’re early-stage, single-provider, and your routing or retry needs are basic.

Where does a payment management system fit into your stack?

Keep in mind that a payment management system doesn’t replace your PSP or acquirer. It’s not automatically a fraud tool or a magic approval-rate fix. These tools give you control and observability, but issuer declines can still happen even with perfect routing and clean logic.

Even with strong routing and retry governance, some issuer declines remain out of your control. Hence, many merchants pair payment management with payment retry automation via a recovery layer that can take eligible declines and convert them into settled revenue behind the scenes.

In practice, a payment management system helps you control the attempt (such as providers, routing, retries, reporting), while a recovery layer focuses on converting eligible issuer-declined card transactions into settled revenue.

Comparison table: Best payment management systems compared

How we compared these tools

We compared these tools using the same criteria so you can shortlist the best fit. Our evaluation is based on publicly available information as of April 2026, including factors like official documentation and release notes. We reviewed:

- Vendor docs, feature pages, and implementation guides

- Supported PSPs/acquirers, payment methods, and key integrations

- Pricing pages and plan limits (or packaging notes where pricing isn’t public)

- Changelogs and release notes (when available)

- Security and compliance posture (e.g., PCI) where relevant

- Third-party reviews and credible comparisons

We focused on the capabilities that matter operationally for scaled merchants, including:

- Control: routing logic, retries, failover, and governance

- Adoption: integration complexity, SDK availability, and maintainability

- Coverage: connectors, payment methods, and global expansion support

- Ops and finance visibility: monitoring, reconciliation, reporting, alerts, and other factors that support downstream analytics like marketing attribution

- Value: pricing transparency and packaging

We didn’t run hands-on tests for every platform. If a capability wasn’t clearly documented, we flagged this uncertainty in the write-up.

15 Best payment management systems for 2026

1.Primer

Primer is a payment management layer (often positioned as “unified payment infrastructure”) that helps merchants centralize provider connectivity, routing logic, and checkout configuration under one integration.

Main features:

- No-code Workflows to route payments based on your logic

- Universal Checkout SDK for web and mobile that unifies methods and processors

- Operational tooling, like monitoring and reconciliation modules

Pricing: By inquiry.

Best for: Merchants who want no-code control over routing and payment method rollout, plus a unified checkout layer.

2.Paymend

Paymend is a specialist approval-rate recovery engine you layer alongside a payment management system. It uses intelligent payment routing and issuer-aware retries to convert eligible declines into settled revenue.

Paymend steps in when routing and retry governance still leaves you with issuer declines you can’t (or shouldn’t) push through on your own merchant accounts.

This solution is most valuable when dealing with generic issuer declines (e.g., “do not honor”), false fraud or security flags, and other issuer risk decisions where customer intent is real but approval confidence is missing.

With Paymend, you can settle more revenue and achieve higher realized conversion without changing checkout UX.

Main features:

- Approval rate recovery engine: Converts eligible declined card transactions into successful approvals

- Full-liability model: Paymend takes ownership of declined transactions, retries them on Paymend’s own infrastructure, and assumes fraud liability for what it runs

- Merchant control over what gets sent: You decide which declines to route to Paymend

- Fast API integration alongside your stack: Designed to sit on top of existing gateways/processors with zero checkout changes

Pricing: No-win, no-fee (Paymend only earns a fee on successfully recovered revenue).

Best for: Merchants losing revenue to issuer declines (especially false declines) that they can’t safely push through on their own accounts. Hence, they want a full-liability recovery layer that retries declined card transactions.

3.Gr4vy

Gr4vy is a cloud-native payment orchestration platform for enterprise merchants and platforms. It’s designed to connect multiple PSPs, payment methods, and tools through a single layer, with no-code rules for routing and retries.

Main features:

- Single integration to a large ecosystem of payment methods and providers

- No-code routing and retry rules

- Tokenization and PCI posture

Pricing: By inquiry

Best for: Enterprise merchants and platforms that need a cloud-native orchestration layer with strong governance.

4.BR-DGE

BR-DGE is a payment orchestration platform that sits between your storefront or app and your PSP(s), providing a single layer for managing routing, resiliency, and payment-method expansion.

Main features:

- Intelligent routing and real-time redirects

- Built-in resilience and secondary gateway failover

- Centralised tokenisation and vaulting aimed at reducing provider lock-in

Pricing: By inquiry.

Best for: Teams optimizing for resilience and uptime protection.

5.APEXX

APEXX positions itself as a payment orchestration platform for complex payment ecosystems, built around a single integration plus tooling for routing and consolidated reporting.

Main features:

- Dynamic routing to route transactions to the optimal acquirer

- Smart Split for controlled traffic splitting

- Consolidated reporting aimed at reducing manual reconciliation across multiple processors

Pricing: By inquiry.

Best for: Merchants that want to optimize acquirer performance with controlled experimentation, especially via traffic splitting.

6.Paydock

Paydock is an API-first payments orchestration platform positioned around plug-and-play connectivity. This solution is designed to connect payment, fraud, identity, and authentication services through a single layer.

Main features:

- Single-API connectivity and dashboard

- Configurable routing by currency, country, scheme, network, and more

- PCI DSS Level 1 token vault

Pricing: By inquiry.

Best for: Merchants that want a composable payments layer that connects payments and authentication services.

7. Inai

inai offers payment orchestration, along with adjacent layers such as monitoring and reconciliation. It’s positioned for merchants expanding geographies and payment methods without a heavy engineering lift.

Main features:

- Orchestration coverage and adaptive routing

- Payment monitoring and alerts to track anomalies

- No-code integrations with major processors

Pricing: Starter tiers begin at $99/month. Growth tiers are by inquiry.

Best for: Mid-market merchants who want orchestration, monitoring, and reconciliation in one place.

8. Akurateco

Akurateco is a payment orchestration platform built for merchants (and payment businesses) that want routing control and broad connector coverage without stitching everything together provider-by-provider.

Main features:

- Intelligent routing and cascading to route and reroute attempts

- Admin panel and customizable dashboard for multi-channel transaction flow

- Deployment flexibility via SaaS, on-prem, and cloud agnostic

Pricing: By inquiry.

Best for: Merchants (or payment businesses) that need broad connector coverage and deployment flexibility.

9. Spreedly

Spreedly is an open payments orchestration platform focused on global connectivity and workflow-driven optimization, built to help merchants and platforms decouple payment logic from any single provider.

Main features:

- Vault that stores credentials and manages token lifecycle

- Optimize workflows for routing and performance visibility

- Level 1 PCI compliant

Pricing: Flex plan starts at $1,500/month; Enterprise is custom.

Best for: Merchants prioritizing vault and token portability to avoid provider lock-in.

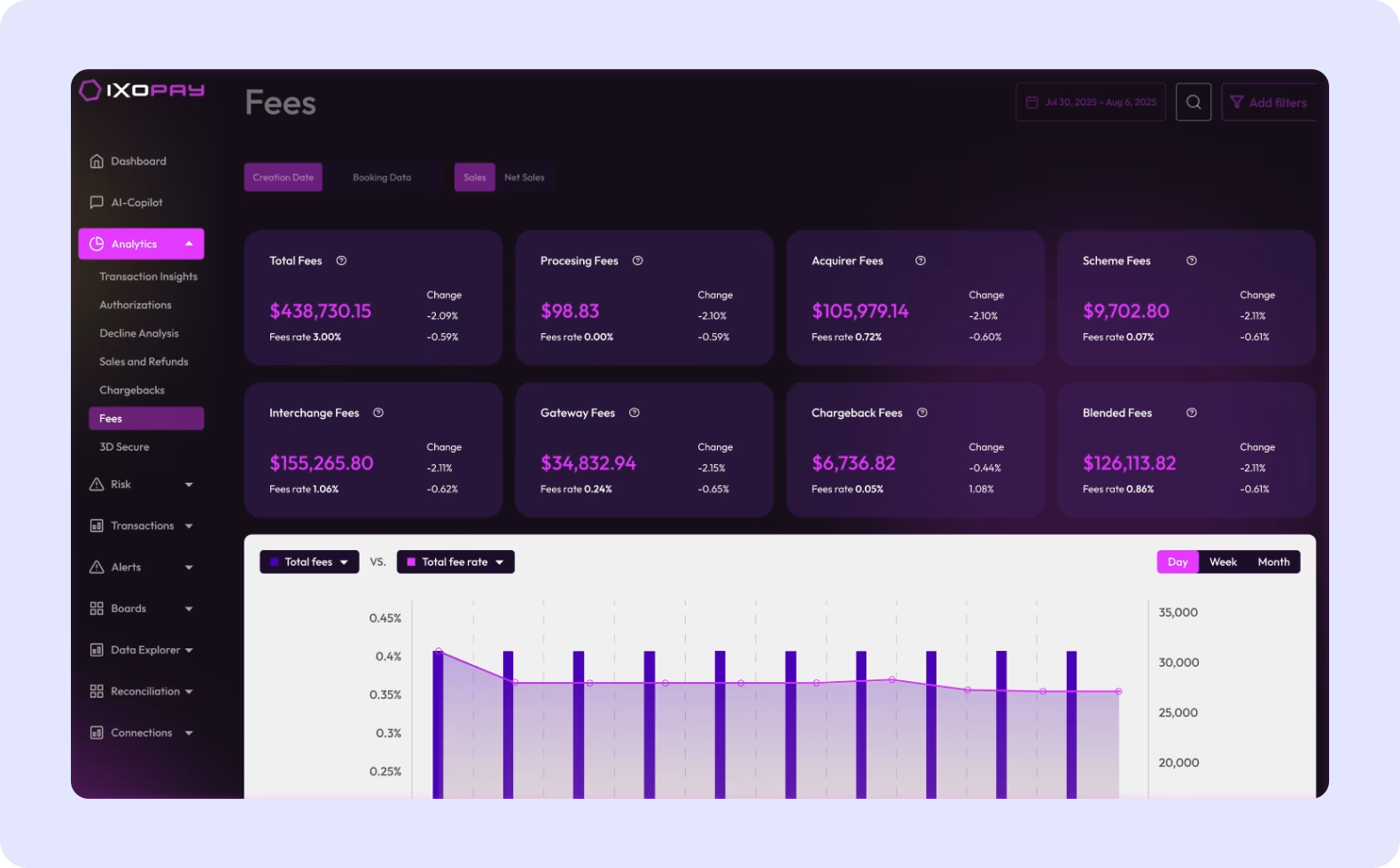

10. IXO Pay

IXOPAY is a payment orchestration platform that combines orchestration with adjacent layers like tokenization and reconciliation. It’s aimed at merchants running multi-PSP stacks and multiple channels.

Main features:

- Single integration across multiple PSPs

- Tokenization layer (“Universal Tokens”) positioned for portability

- Reconciliation and settlement tooling as part of the orchestration stack

Pricing: €199/month (Starter) and €499/month (Growth)

Best for: Merchants that want orchestration and an ops layer for tokenization and reconciliation workflows.

11. Neodeos

NeoDeos is a payment orchestration platform designed for merchants and payment institutions that want a single API and dashboard to connect providers and manage payment operations centrally.

Main features:

- Single-API orchestration across providers and payment methods

- Smart routing and fallback with configuration options

- Consolidated analytics and reporting across providers and payment methods

Pricing: By inquiry.

Best for: Teams that want a simple “one API plus one dashboard” approach to orchestrating multiple providers.

12. Yuno

Yuno is a global payment orchestration layer designed to centralize providers, payment methods, acquirers, and fraud tools behind a single integration. So, payments teams can scale into new markets without rebuilding the stack each time.

Main features:

- Single-API orchestration

- Lifecycle coverage across checkout, authorization, routing, fraud prevention, settlement, and reconciliation

- Smart routing and localization

Pricing: By inquiry.

Best for: Merchants expanding internationally who need broad local payment method coverage and localization.

13. TNSI

TNS Orchestrate is a cloud-native payment orchestration platform built for enterprise and unattended merchants, positioned around omnichannel acceptance and multi-acquirer routing.

Main features:

- Omnichannel orchestration across in-person, online, and unattended payments in one platform

- Single integration and developer tooling

- Central dashboard and real-time visibility

Pricing: By inquiry.

Best for: Omnichannel and unattended payments use cases, where orchestration must span multiple environments.

14. Payrails

Payrails positions itself as a modular payments operating system that combines payment orchestration, tokenization, reconciliation, and analytics to replace fragmented payment logic and financial workflows with one integration.

Main features:

- Token vault and proxy

- Automated reconciliation and unified analytics

- Chargeback management and payouts modules

Pricing: By inquiry.

Best for: Merchants that want a more modular payments operating layer.

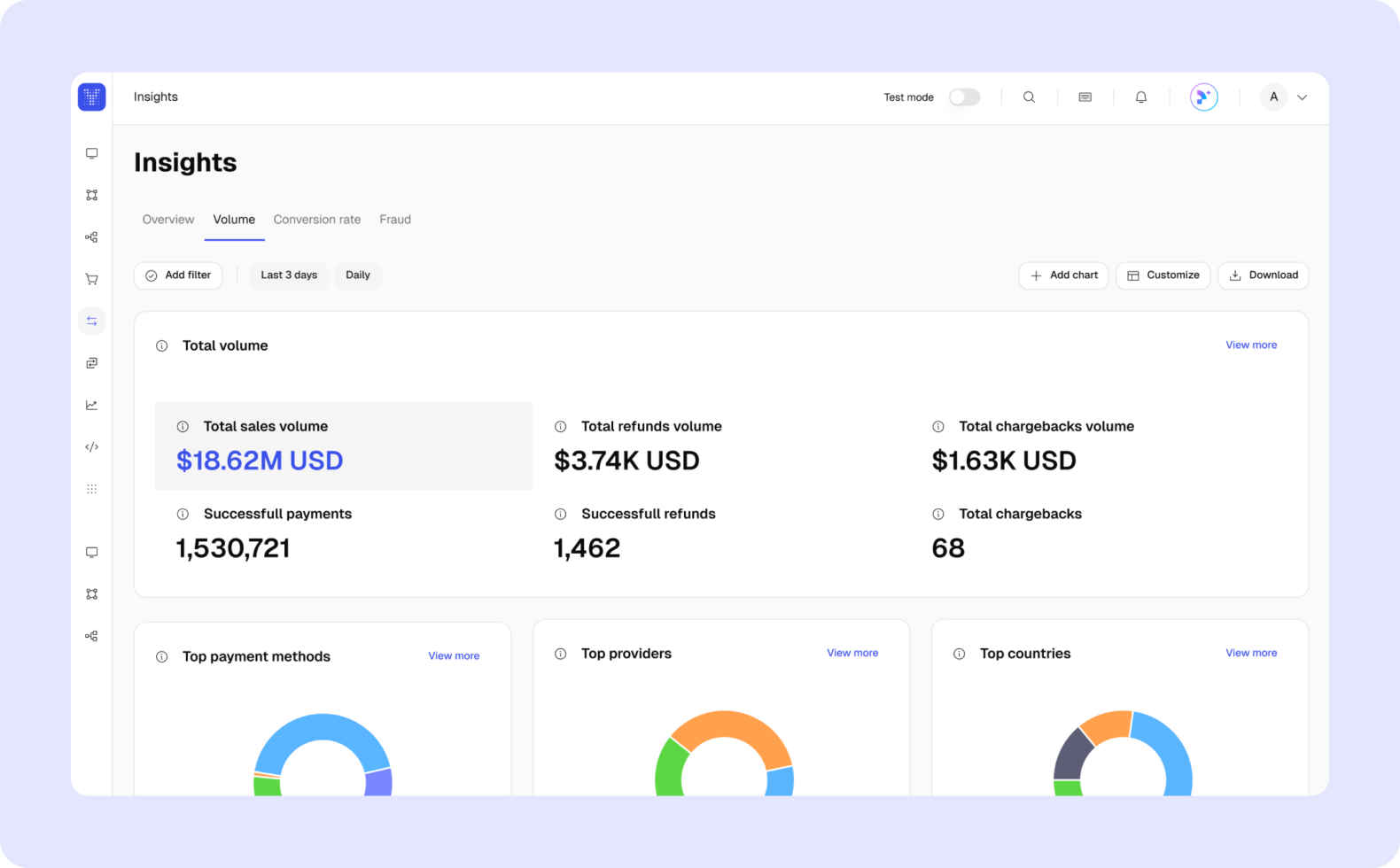

15. ProcessOut

ProcessOut is a payment analytics and routing platform focused on giving merchants control over provider performance through monitoring and a vault. For teams automating payment ops, this kind of routing and performance layer can also support an AI agent that monitors anomalies and recommends (or triggers) routing changes.

Main features:

- AI Smart Routing, positionined as learning-based routing beyond static rules

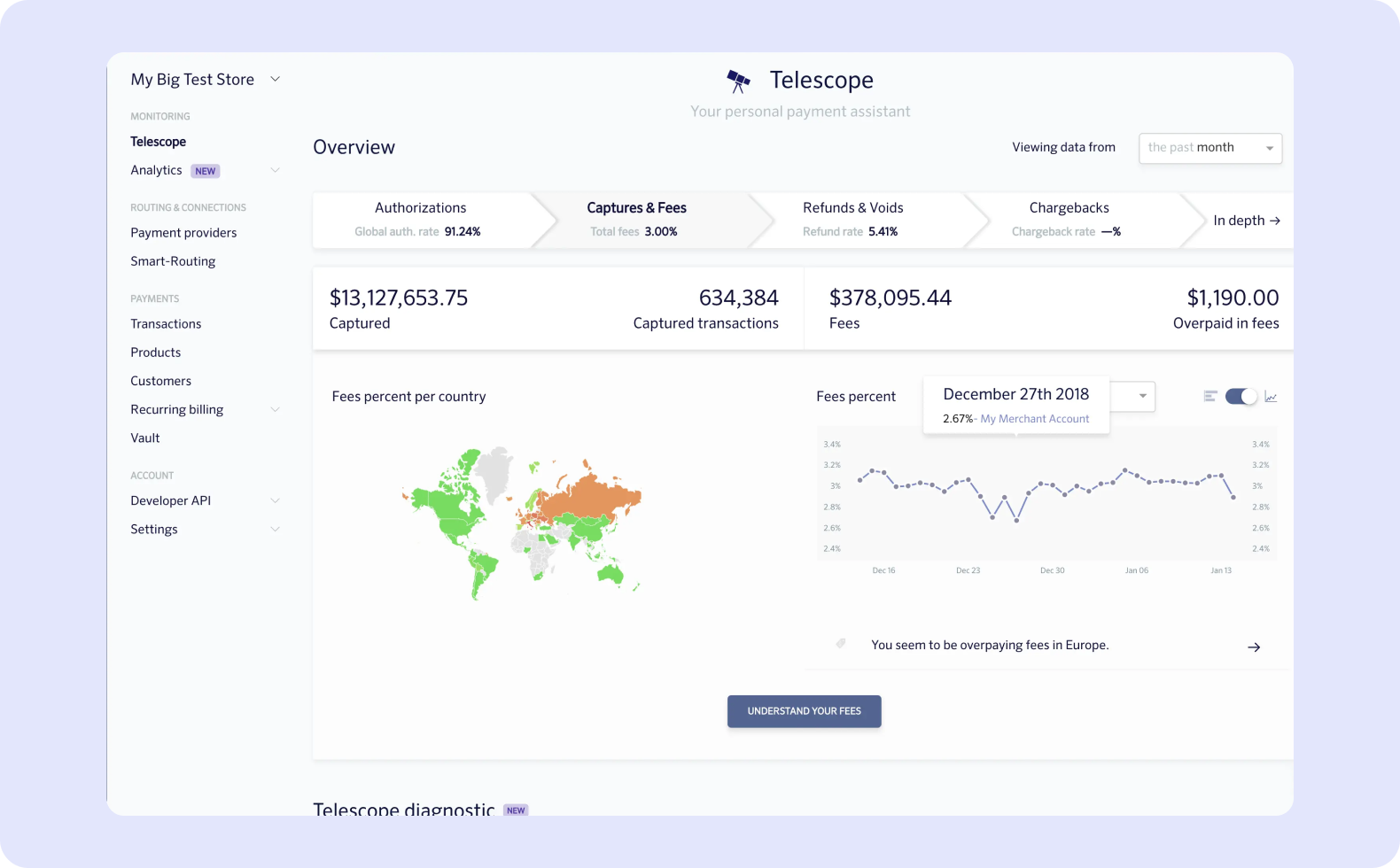

- Monitoring (Telescope) to analyze transactions across providers

- PCI-compliant vault and network tokens

Pricing: Basic plan free; advanced plans paid.

Best for: Merchants that are analytics-led about payments, and are looking for better monitoring and visibility.

From payment ops to recovered revenue

Payment management systems give you leverage like multi-provider resilience and reporting that your finance team can actually trust. These solutions help scaled merchants prevent payment operations from becoming a constant cycle of one-off fixes.

But even the best orchestration layer won’t eliminate issuer declines on its own. Issuers can still reject legitimate card-not-present transactions. Hence, you still need to consider how to achieve more settled revenue from the same demand, without widening risk.

Paymend is the layer you add after your payment management system when you want to recover eligible declined card transactions you can’t (or shouldn’t) push through on your own merchant accounts. Paymend retries those declines on Paymend’s own infrastructure, assumes fraud liability for what it runs, and works behind the scenes with zero checkout changes.

If your priority for 2026 is more settled revenue from the same demand, without increasing fraud exposure, book a Paymend demo.