.avif)

Intelligent payment routing is supposed to turn declines into approvals. But declines aren’t random—they cluster by issuer, region, BIN ranges, velocity patterns, and the false positives your fraud tooling creates. That’s why intelligent payment routing can’t just mean adding an acquirer. It has to mean making better decisions with better signals.

Most online payment failures still come down to issuer decisions made with limited card-not-present context. A meaningful share of that leakage is false declines: legitimate customers issuers (or fraud filters) incorrectly reject. It’s one reason why 6 in 10 merchants use tokenization to reinforce security and boost authorization rates. However, intelligent payment routing only matters if it turns those false declines into captured, settled revenue.

If payment approvals don’t translate into settlement, you haven’t actually recovered anything. That’s why intelligent payment routing has to be operationally accountable with clear decisioning on when to route, when to suppress, when to retry, and how to measure whether your changes create incremental settled revenue.

What is intelligent payment routing?

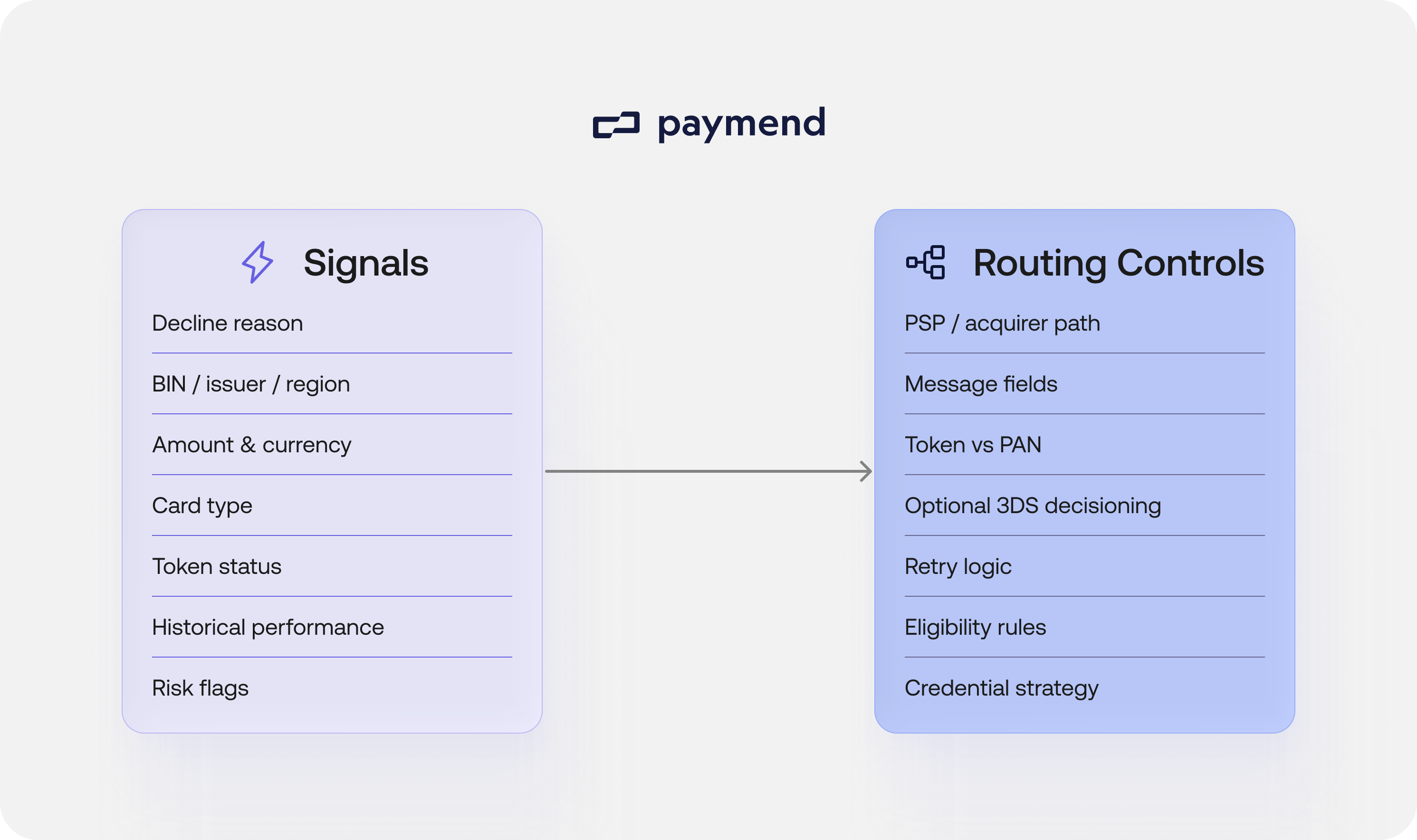

Intelligent payment routing is the decision layer that chooses how a card transaction should be attempted to maximize the chance it gets authorized, captured, and settled. It involves selecting the best execution path and the cleanest way to send the authorization message based on what issuers are actually approving.

At a minimum, it needs inputs like:

- Issuer response signals (e.g., decline reason).

- Bank Identification Number (BIN), issuers, and region patterns

- Amount, currency, card type, and merchant account constraints

- Credential status, such as token availability

- Risk signals (e.g., fraud flags)

Then it makes decisions such as which path to use for the attempt, which credential to present, and how to populate the key authorization fields. Intelligent payment routing also decides whether to retry, when to retry, or when to suppress to avoid issuer fatigue.

If done well, intelligent payment routing should classify the decline, take the next-best action, and measure outcomes at the issuer level. Done poorly, it’s an expensive failover that trains issuers to decline and inflates costs without improving settled revenue.

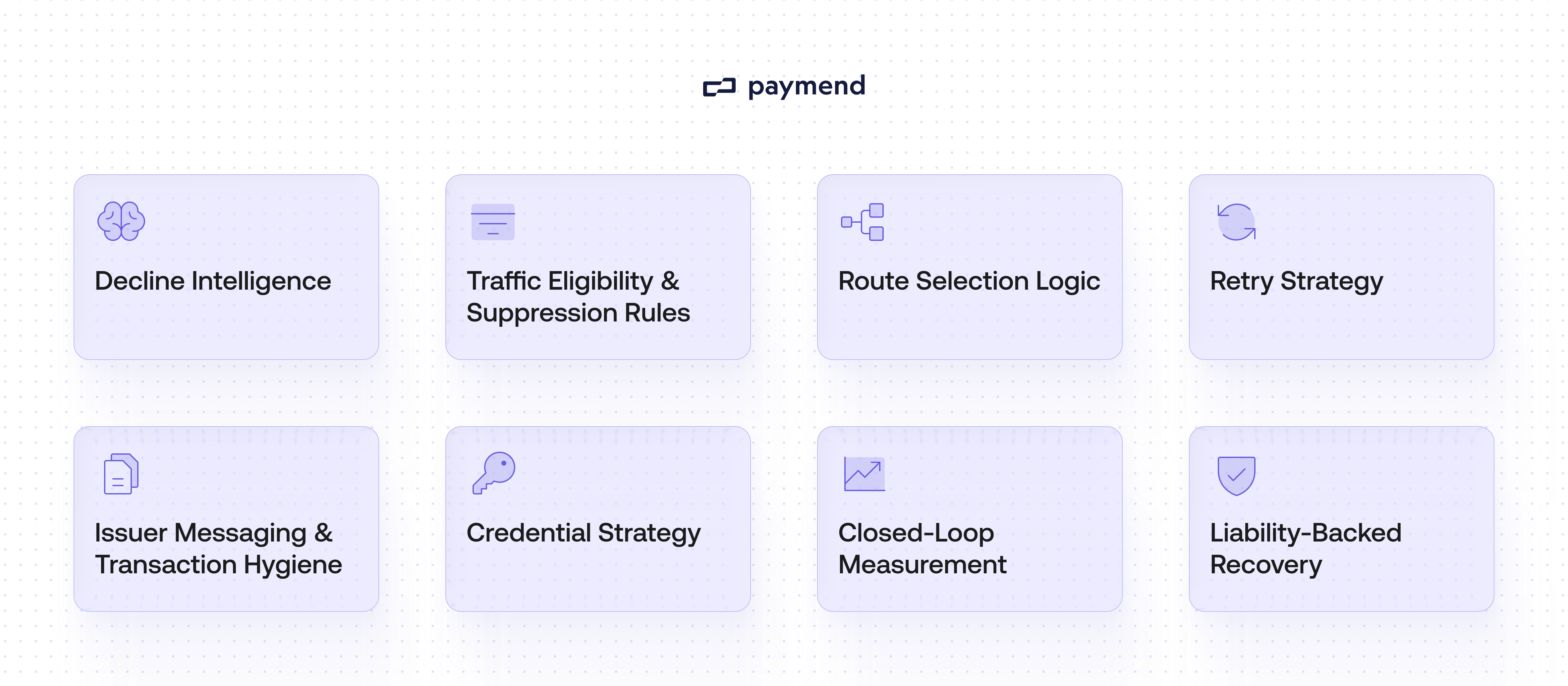

8 Essential components for intelligent payment routing

These eight components show what intelligent payment routing looks like in practice, and why most routing stacks plateau.

Component 1: Define intelligence

Decline intelligence is the translation layer between issuer responses and routing actions. For this component, you need to define a decline taxonomy that maps cleanly to decisions:

- Fixable now = issues you can correct immediately (e.g., duplicate detection).

- Try later = outcomes that improve with timing or sequencing (e.g., issuer velocity windows).

- Suppress = hard stops where additional attempts waste cost and can hurt your account health (e.g., invalid account).

Then, you’ll be ready to improve classification with patterns issuers actually follow. For example, the same generic decline or response code (e.g., Do Not Honor) can have different root causes depending on issuer behavior. Or, some issuers and fraud systems are more restrictive during certain times of day. The point of classification is to reduce wasted recovery attempts and reallocate effort toward declines.

Component 2: Traffic eligibility and suppression rules

Routing without eligibility controls can quickly slip into ‘try anything’ territory, and issuers may punish that. Done right, eligibility and suppression rules support your wider brand protection strategy by preventing noisy repeat attempts that frustrate customers and trigger issuer pushback. It’s important to build explicit eligibility rules that determine which transactions should enter your routing and retry logic:

- Transaction type controls, such as recurring vs one-off.

- Customer context, like prior successful payments.

- Amount or currency thresholds as needed because high-value attempts often require tighter guardrails.

- Risk posture through visibility over velocity signals and anything that correlates with disputes.

Cooldown windows and kill switches that automatically suppress attempts are useful guardrails to prevent issuer fatigue. You could also set a maximum attempts limit per transaction or card, and stop bursts by issuer, BIN, or cohort when declines spike.

Here’s an example: you might suppress lost/stolen and cap ‘Do Not Honor’ retries to X attempts in Y hours to avoid issuer pushback and monitoring risk.

Component 3: Route selection logic

Route selection is all about choosing the best execution path for a particular attempt. There are many factors to consider, including issuer-level outcomes (e.g., approvals), the geography and currency fit, the card type and scheme behavior, and the payment amount bands. Operational constraints, such as settlement timing and processor limits, also play a role.

Two things make route selection stay intelligent over time:

- Periodically re-testing routes in a controlled volume.

- Monitoring issuer behavior shifts and automatically downgrading routes that regress. This only works if you treat routing like an operating program with clear ownership and basic resource management.

You’ll be able to spot good routing in production, as it will show up as stable logic, controlled experimentation, and decisions justified by measured outcomes. Route selection stays intelligent only if you continuously re-test and monitor drift.

Component 4: Retry strategy

Importantly, retries can be sensitive. They’re a controlled strategy with timing, spacing, sequencing, and stop conditions. You can build retries around decline classes, including:

- Immediate retry = only for true transients, like processor timeouts, where the same attempt is likely to succeed minutes later.

- Delayed retry = for declines where issuer sensitivity can change with time windows.

- No retry = hard do-not-retry signals and clear fraud-related hard stops.

When designing these decline classes, you could consider elements like stop rules that cap attempts when signals indicate further attempts won’t convert, and sequencing that decides whether a retry should perform an action such as switching the route.

Be sure to measure approvals per attempt so you can see if it drops. Keep in mind that undisciplined retries train issuers to decline and can degrade performance over time. Controlled retries do the opposite: they convert only what’s realistically recoverable.

Component 5: Issuer messaging and transaction hygiene

Transaction hygiene is a crucial prerequisite for routing performance. Specific hygiene fields include stored credential flags, consistent descriptors, and MIT indicators. If the authorization message is inconsistent, routing can’t save it. The goal of this component is to remove avoidable ambiguity, so issuers don’t default to decline due to messy signals.

Hygiene refers to factors like stable transaction metadata so issuers can recognize legitimate patterns, accurate flags for merchant-initiated vs customer-initiated behavior, and clean customer data. After all, routing can’t recover revenue if credentials are stale.

Component 6: Credential strategy

You’d be surprised how many declines are preventable credential problems. Credential strategy is about reducing avoidable failures caused by stale or fragile credentials while keeping the buyer experience unchanged. For example:

- Use network tokens where available to improve credential stability.

- Handle expiry updates and credential refreshes using lifecycle management.

- When token provisioning fails, use fallback logic.

- Deduplication, consistent identifier mapping, and clean storage practices help with vault hygiene.

Tracking credential KPIs can help you identify factors like token and refresh success rates.

Component 7: Closed-loop measurement

If you only track approval rate, you’ll miss the real question: Did you actually settle the payment? Closed-loop measurement means you measure routing decisions all the way through to the outcome that matters. In practice, this starts to look a lot like retail data analytics: joining payment outcomes to customer cohorts and product-level patterns so you can see where you lose revenue.

As a minimum, you should measure:

payment attempt → payment authorized→ payment captured (or sent for clearing) → payment settled.

You can also consider the net revenue impact and risk outcomes, such as chargeback exposure. Use holdouts (or challenger and control routing splits) so you can prove incremental lift. Then add drift monitoring by issuer/BIN so you can downgrade a route quickly, not after the month-end close.

You have the option to make decisions by route, decline type, issuer, BIN, region, attempt number, credential type, and more. It’s worth noting that intelligent payment routing might improve payment approvals, but these may still fail later at the capture or settlement stages, or increase risk outcomes you don’t see until weeks later.

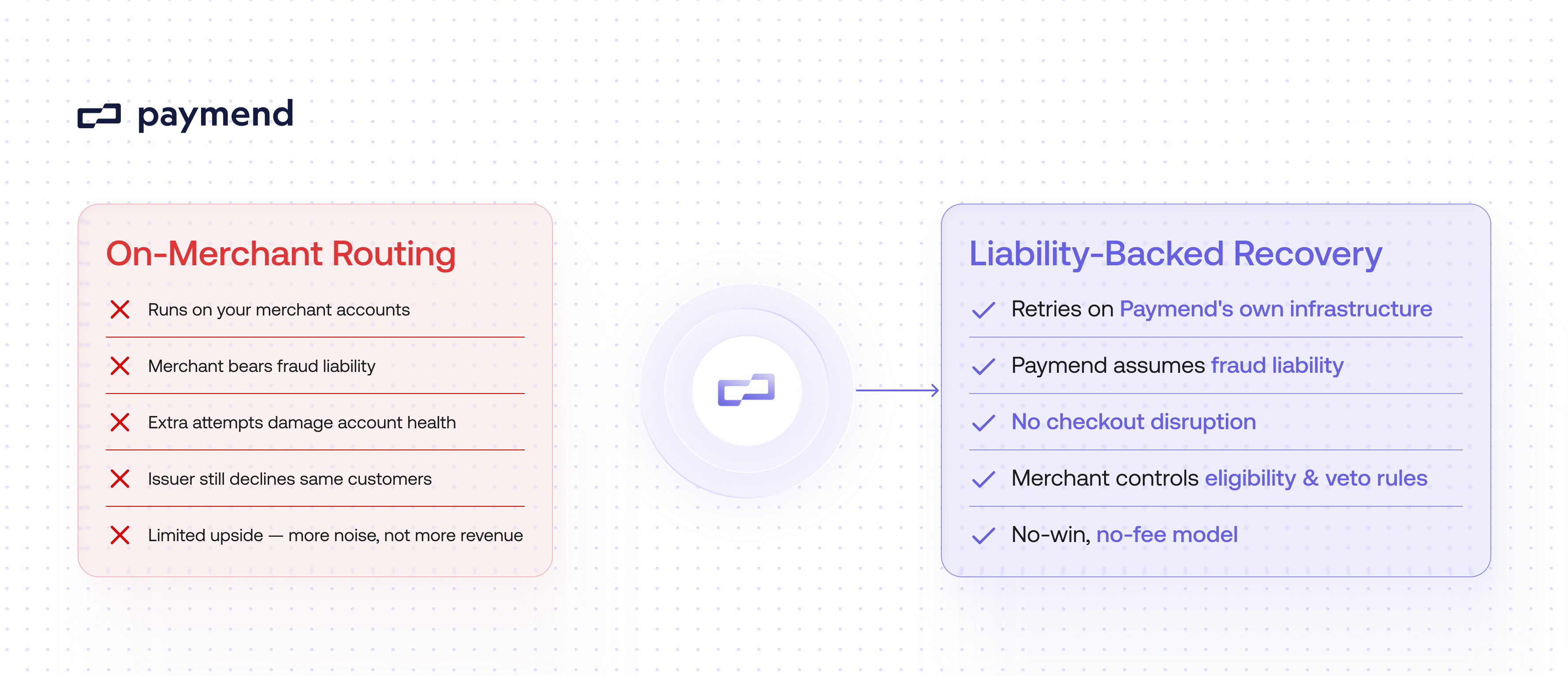

Component 8: Liability-backed recovery when routing hits a ceiling

Even the best intelligent payment routing stops working if routing inside your stack still runs on your merchant accounts, with your risk profile and constraints. You’ll notice you’ve hit a ceiling when the issuer keeps declining the same good customers, even after you’ve cleaned up messaging and exhausted retries. Or, you can’t do any more without increasing fraud exposure on your merchant accounts. You may also find that any additional attempts start to harm your merchant account health.

At this point, you can reconsider who owns the next attempt. This is where liability-backed recovery fits. Instead of retrying forever inside your own stack, merchants can hand off eligible declined card transactions to a payment recovery engine like Paymend. Keep in mind that this component isn’t ‘more retries on your account.’ It’s recovery with risk ownership.

For example, Paymend then retries those declined card payments on Paymend’s own infrastructure, assuming fraud liability and working the transactions through to settlement with no checkout disruption. You stay in control with eligibility rules and veto logic. Paymend only earns when revenue is successfully recovered in a no-win, no-fee model. It’s a different commercial lever: recovery with risk ownership.

Measure what settles, not what authorizes

Intelligent payment routing is a system, not a single feature. If you are looking for durable lift, you need all eight components working together, from clear decline intelligence to measurement that ties every change back to incremental settled revenue.

The practical goal is simple: recover more revenue without increasing fraud exposure or damaging account health. And when routing hits a wall, such as if the issuer keeps declining and more attempts start to create noise, don’t force it. Add a second lever: liability-backed recovery. With Paymend, you can hand off eligible declined card transactions, and Paymend retries them on its own infrastructure while assuming fraud liability.

With Paymend, you can convert false declines into settled funds with no checkout disruption. Find where retries stop being profitable and turn them into revenue by getting in touch with the Paymend team.