Every declined card payment is revenue you were entitled to collect—right up until it doesn’t settle. For finance and payments teams, that means lost forecast accuracy and missed CAC payback targets, along with the erosion of lifetime value from customers who had every intention of paying.

Online card approvals are constrained by issuer risk decisions and limited card-not-present visibility, and issuers make authorization decisions based on risk signals that do not always reflect reality. The result is a steady stream of legitimate transactions that never reach settlement.

Fortunately, there is a viable solution for many declined payments. Payment retry automation is the logic that determines when, how, and whether a declined transaction gets a second attempt. It’s a disciplined, data-driven process aimed at recovering revenue from transactions declined for fixable or ambiguous reasons. Recent studies show that over 90% of merchants use approaches to boost authorization rates, with automatic retries as one of the most common tactics.

The challenge is that standard retry logic has limits. If you are retrying on the same merchant accounts with the same risk profile, many declines will not flip regardless of how well your rules are configured. Getting past those limits requires understanding both how retry automation works and where it hands off to more advanced payment recovery approaches. Let’s take a closer look at what payment retry automation is and how it works.

What is payment retry automation?

Payment retry automation is the systematic re-attempt of a declined card transaction through your payment gateway using predefined logic, with no manual intervention required. The goal is to recover otherwise-lost revenue by identifying declines that are likely to resolve on a subsequent attempt and acting on them intelligently. It’s important to note that this process is not about spamming customers with repeated charge attempts.

Why card payments get declined

A decline response is generated by the issuing bank, the payment network, or sometimes the processor or acquirer before the request even reaches the issuer. The reasons range from suspected fraud and velocity limits to technical timeouts and generic “do not honor” responses, which are catch-all codes that can mean almost anything. The issuer’s decision is final in real-time, which is why understanding the decline context is so important before deciding how to respond.

Soft declines vs. hard declines: What actually gets recovered

Not all declines are created equal. Hard declines are usually stop conditions. Retrying them rarely helps unless you have evidence that the code is being misclassified upstream.

Invalid account numbers, lost or stolen card flags, and confirmed fraud blocks fall into this bucket. Retrying them increases decline velocity without any prospect of approval, which can negatively impact your processing reputation.

Soft declines are where recovery is possible. These include technical timeouts, issuer-side risk decisions that can shift with timing or routing changes, and the notoriously vague “do not honor” responses that require disciplined testing to classify. Good retry automation separates these categories cleanly and applies different logic to each.

When you need a recovery engine as part of your payment retry automation strategy

Standard payment retry automation has real limitations, and understanding them is key to knowing when a different approach is needed.

Basic retries happen on the merchant’s existing gateway, acquirer, and merchant ID (MID). You can add retry attempts, adjust timing, and refine your rules, but you cannot change the underlying reasoning that caused the issuer to say "no" in the first place.

Many decline codes are generic and inconsistently applied across issuers and processors. In practice, they lead rules-based retry automation setups to over-retry or under-retry the declined payment. Retrying risk-driven declines without strong gating can increase card fraud and chargeback exposure.

When you are dealing with scenarios such as elevated fraud-related declines, a high volume of generic "do not honor" responses, scaling caps, or routing complexity, standard retry logic cannot recover the revenue on its own, and a payment recovery solution is required.

The recovery engine difference

A payment recovery engine is a dedicated layer designed to pursue the declines that standard retry logic cannot flip. Most recovery engines offer more sophisticated retry logic than a basic setup, but the most advanced solutions go further.

Rather than retrying on the merchant’s own infrastructure, they process those attempts on their own merchant accounts and banking setup. Retries run off your MID, and Paymend assumes fraud liability for the transactions it processes. Recovery runs silently in the background with no checkout disruption and no customer re-authentication required.

The result is more settled revenue from transactions that would otherwise be written off, without taking on additional fraud exposure.

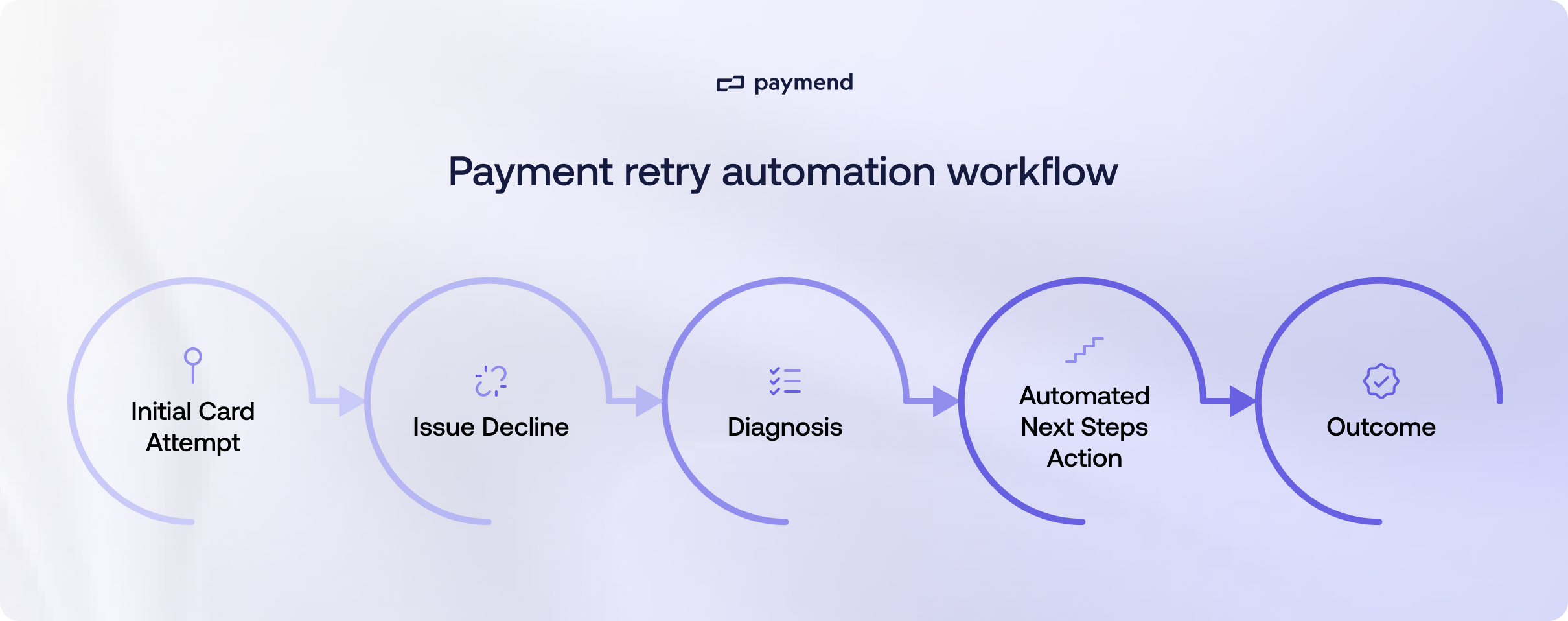

Step-by-step: How payment retry automation works with a recovery engine

Here is how payment retry automation works in practice when paired with a recovery engine, from the moment a decline is logged to the point where revenue is either recovered or ruled out:

Step 1: A decline happens and gets surfaced

When a card transaction is declined, the merchant’s payment stack logs the attempt and captures the associated metadata. This metadata determines how precisely you can diagnose the decline and act on it.

Ideally, you capture:

- The issuer response code and reason, at the most granular level available.

- Network response details, where exposed.

- Processor and acquirer metadata, including whether the failure was a hard stop or a timeout.

- Context flags like first attempt vs. recurring charge, and card-on-file vs. customer-initiated

- Transaction context: amount, merchant category code (MCC), region, velocity

- Prior approval history for that card or customer fingerprint

The richer this dataset, the more precise your recovery logic can be.

Step 2: The merchant selects what gets sent to the recovery engine

Not every declined transaction is a candidate for recovery, and merchants retain full control over what gets escalated. Eligibility rules define the traffic that gets routed to the recovery engine, filtering by decline type, transaction amount, geography, customer cohort, or any other criteria that make sense for the business.

Eligibility rules can also reflect your security risk tolerance, so higher-risk cohorts never enter recovery. This selective approach is one of the key strengths of a recovery engine model. You decide what to send, and nothing moves forward without your rules being satisfied first.

Step 3: Paymend ingests the declined transaction via API

Eligible declined transactions are passed to Paymend through an authenticated, secure API integration that sits alongside the merchant’s existing payment gateway and payment stack. There is no checkout disruption at this stage or at any other point in the process. The entire recovery workflow runs silently in the background, invisible to the customer and requiring no re-authentication on their end.

Before Paymend accepts a transaction into its recovery workflow, the platform applies its own risk gating. If a transaction does not meet the designated thresholds (for example, because it carries signals that point to genuine fraud rather than a recoverable decline), the platform can veto it, which protects both the merchant and the integrity of the recovery process.

Step 4: Diagnosis and next-best-action decisioning

Paymend's engine interprets the decline context by analysing issuer behavior patterns and classifying the decline into one of three categories:

- Error: a technical or processing failure that is likely retryable.

- Risk flag: a decline driven by fraud or risk signals that requires careful evaluation before any retry.

- Ambiguous: a generic response such as "do not honor" that requires pattern analysis to determine the best course of action.

The decline context feeds into the next-best-action decisioning output: whether to retry, when to retry, and when to stop.

Step 5: Recovery execution on Paymend's own infrastructure

Unlike smart retry tools that only re-attempt declined transactions on the merchant’s own MID, Paymend takes a different approach. Retries are processed on the platform’s own merchant accounts and banking setup, so the issuer sees a different context entirely.

This difference changes the outcome for declines that would otherwise keep failing.For the merchant, recovery happens without adding any risk to their existing payment setup. Paymend assumes fraud liability for the transactions it processes, so recovery doesn’t add fraud liability to your merchant account.

Step 6: Reporting, reconciliation, and outcome measurement

For finance teams, the metrics that matter most at this stage are recovered revenue, recovery rate on eligible declines, and settlement and reconciliation outputs that slot cleanly into existing workflows without creating manual exceptions. Finance can tie this directly to customer acquisition cost (CAC) payback by measuring how much recovered revenue comes from newly acquired cohorts versus mature accounts.

Once recovery activity is complete, these metrics are visible in Paymend’s real-time reporting dashboard. The platform works on a “no-win, no-fee” basis. It only charges a fee on revenue it successfully recovers, so if nothing is recovered, there is no cost. The ROI is straightforward to measure and easy to justify internally.

Where payment retry automation ends, recovery begins

Payment retry automation is a powerful tool for recovering revenue from declined transactions, but it has real limits. When retries happen on the merchant’s own infrastructure, the underlying constraints that caused the decline don’t change. Getting past those limits requires a more advanced approach, which is where payment recovery engines come in.

Paymend is a revenue recovery platform for declined card transactions. It takes end-to-end ownership of eligible declined card transactions and retries them on its own infrastructure without exposing the merchant to additional risk. It integrates through an API that doesn’t disrupt checkout, and its “no-win, no-fee” pricing means the platform only earns on recovered revenue. Book a demo to see what Paymend would recover from your last 30 days.