Payment declines don’t always feel like a strategy problem. They feel like noise. But when approvals slip, everything downstream becomes more expensive: conversion rates drop, and customer acquisition costs rise.

That’s why the merchant account vs payment gateway decision matters. The choice affects how your payments operation performs day to day, from risk tolerance to how quickly you can respond when issuers start rejecting good transactions.

And the stakes are only increasing. 77% of payment executives identified e-commerce growth as the critical driver accelerating the shift to non-cash transactions, meaning more revenue is now won or lost inside online card acceptance infrastructure.

What is a merchant account?

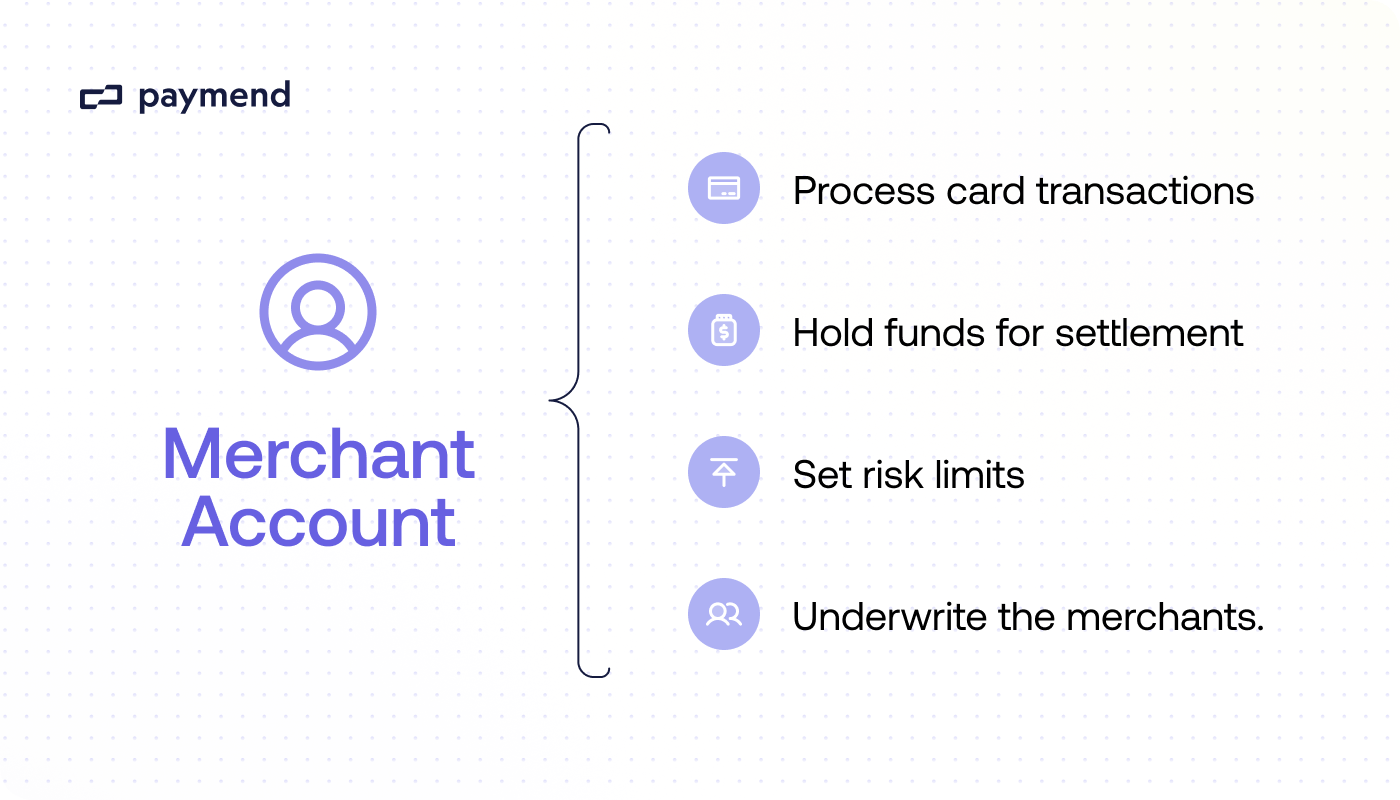

A merchant account is the acquiring setup and MID that your processor or acquirer uses to submit payment authorizations and settle funds. It also defines how approved transactions are captured, settled, and paid out to you.

Your merchant account setup and history shape what issuers see in the authorization message and how they evaluate risk. That means the account can influence approval outcomes (and false declines), not only pricing or settlement timing.

Merchant accounts also come with underwriting and ongoing monitoring. Expect risk controls like velocity limits and chargeback thresholds. These constraints affect factors such as what you can process and how resilient your payments operations are under load or during risk events.

What is a payment gateway?

A payment gateway is the software layer that securely collects card details at checkout and sends the transaction data to your processor and acquirer for authorization. It returns approval or decline responses in real time and handles the mechanics of reliably passing data back and forth.

In practice, payment gateways also manage things like tokenization and payment form components (e.g., hosted fields). Many gateways also bundle extras, such as stored payment methods, webhooks, basic fraud tooling, and analytics.

A gateway doesn’t settle funds on its own. Settlement and payouts still depend on your underlying merchant account. That’s why, in most setups, you’ll use a gateway alongside an acquiring or merchant account, even if one provider bundles them in one product.

Operationally, gateways also influence factors like latency and data completeness, which affect payment approval outcomes at the margin. This happens through technical failures (e.g., timeouts) or weaker authorization signals reaching the issuer.

Gateways can also be the layer that makes redundancy practical, by simplifying how you add processors or fail over when one path degrades. From an ops perspective, that redundancy is part of IT service continuity, ensuring payments keep running even when a provider or route is degraded.

Here’s a quick side-by-side to make the differences concrete.

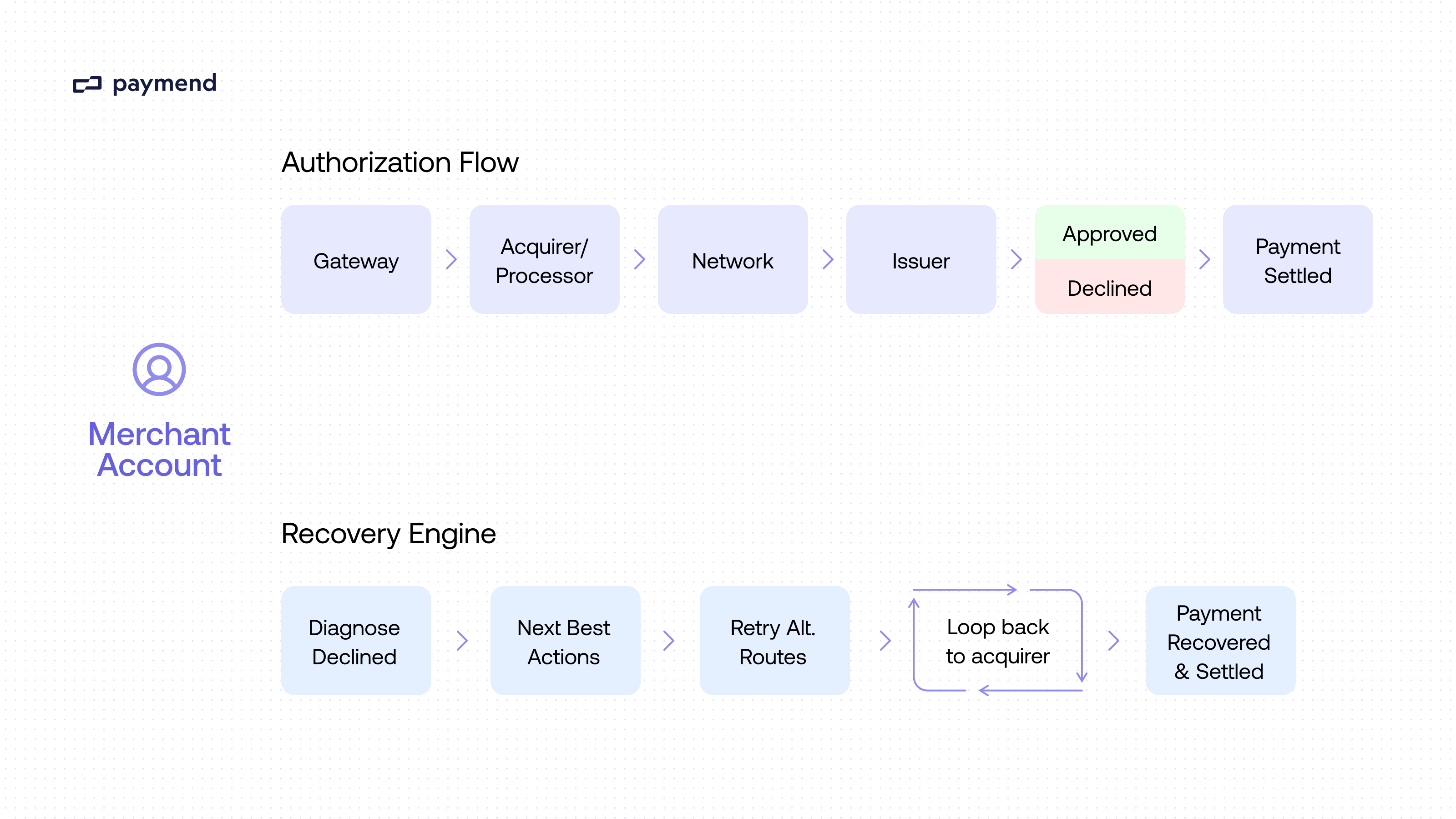

Merchant accounts vs payment gateways: Where do they sit in the payment authorization flow?

Here’s the typical card-not-present payment authorization path:

- Customer submits payment: Card details are entered (or a tokenized stored credential is used).

- Payment gateway captures and secures the payment data: Encrypts or tokenizes where relevant, and packages the transaction payload. Then, it sends the request onward to processing.

This is where the payment gateway matters. Timeouts tend to show up as technical failures. For example, the issuer may never see the request. And if stored-credential or token indicators are passed inconsistently, issuers get weaker signals, which can increase uncertainty and declines.

- Processor or acquirer submits the authorization using an acquiring setup: The transaction runs under your MID (or, in an aggregated model, your provider’s MID with you as a sub-merchant).

At this point, the authorization runs under the issuer-facing footprint. The merchant account matters here because your underwriting profile and MID history influence what gets through and what issuers see when they decide to approve or decline.

- Card network routes to the issuer: The network passes the request to the cardholder’s bank.

- Issuer approves or declines: Decision is returned back through the network → acquirer/processor → gateway.

- Gateway returns the response to your checkout: You get an approval or decline code and can act on it server-side.

- If approved: capture → clearing/settlement → payout: Capture typically happens immediately or later. Funds settle through the acquiring side and pay out to your bank account per your merchant account terms.

Essentially, you’re still using both functions: a gateway to securely transmit transaction data and handle the response loop, and a merchant account to actually run the authorization through an acquirer and settle funds.

Merchant account vs payment gateway: Which is right for you?

It’s important to remember that this isn’t an “either-or” decision. Most online merchants run a gateway and an acquiring or merchant account setup. That’s because the gateway is what securely collects and transmits payment data at checkout, while the merchant account is what actually enables authorization and settlement.

In other words, one moves the information, the other moves the money. Online card payments typically require both functions to complete the loop.

The real question is whether you are looking for cash predictability and risk controls, or speed, flexibility, and portability as you scale. Let’s take a look.

Choose a merchant account-led setup if…

- You need predictable settlement and tighter control over holds. If your finance team cares most about factors like cashflow accuracy, you’ll want an acquiring setup where you can negotiate and manage those levers directly.

- You’re scaling volume and want to leverage processing economics. At meaningful volume, basis points matter. A merchant account-led approach typically gives you more room to push on pricing and optimize by region.

- You have risk or chargeback maturity and want direct relationships. If you can manage underwriting conversations, you’ll benefit from owning the relationship instead of inheriting generic risk policies designed for the median merchant. This is often part of a broader brand protection strategy for the benefit of long-term account health.

Choose a gateway-led setup if…

- You need fast integration and strong developer tooling. When you’re moving quickly, a clean payment gateway integration is usually the quickest way to ship reliably without rebuilding your acquiring setup.

- You want easier support across payment methods and checkout surfaces. Merchants taking payments across multiple channels can benefit from a gateway-led approach to reduce complexity and keep payment logic consistent.

- You value portability and redundancy. Gateways can make it easier to add processors and expand into new regions without re-architecting your stack.

The simplest way to decide: pick the path that best matches your current constraint.

How does your setup influence payment declines?

Payment declines don’t only come from the customer or the issuer. Your gateway and merchant account or acquirer setup shape what signals make it into the authorization request, and whether that request reaches the issuer cleanly and consistently. Good retail data analytics helps you separate issuer declines from technical failures and upstream blocks, so you can fix the right layer instead of guessing.

Some declines never reach the issuer at all. They’re rejected upstream by merchant-side risk rules, gateway constraints, or acquiring risk controls, then surfaced as a generic failure.

For example, if the gateway is timing out, you’ll see more technical failures. If factors like stored-credential indicators are inconsistent, you’re effectively asking issuers to decide with less context.

False declines show up here. What happens is that issuers make probabilistic decisions with limited CNP visibility, so their confidence is heavily influenced by the authorization message and your processing footprint. Even when the customer is good, weak or inconsistent signals, such as MID history and network token performance, push issuers toward “no.”

This problem highlights why merchants struggle to quickly fix false declines internally. Even with a solid gateway and a well-managed merchant account, you’re still operating within constraints such as pre-issuer blocking and merchant account health.

Therefore, issuers still default to declines when they’re uncertain. That’s also why many teams treat recovery as a distinct layer: handling eligible declined card payments after the first attempt, instead of assuming stack tweaks will eliminate the problem.

Where revenue recovery engines fit and why you need one

Revenue recovery engines sit after the first attempt and focus on converting eligible declined card transactions into successful approvals, without asking you to rebuild your gateway or merchant account setup.

This is what most teams mean by failed payment recovery: converting eligible declined card transactions into settled revenue after the first attempt. These solutions are a distinct layer that exists because even well-run stacks still face issuer uncertainty and false declines.

Most retry automation is constrained by your own merchant account risk profile, processing setup, and issuer trust signals. As a result, you can quickly hit diminishing returns (or create downstream risk) trying to brute-force declines from the same footprint.

A revenue recovery engine fits into this landscape by recovering approvals without stressing your own account health or changing checkout behavior. It works by retrying eligible declined card transactions on Paymend’s own infrastructure and assumes fraud liability. It uses intelligent diagnosis to apply the next-best action until funds settle, with merchant control over what gets sent and built-in veto logic for high-risk traffic.

It’s important to note that Paymend doesn’t replace your gateway or acquirer—it sits after the first decline as a recovery layer.

Infrastructure decisions show up in the numbers

It is most likely that you will need both a payment gateway and a merchant account setup. The right infrastructure loosely depends on whether you are optimizing for faster iteration and portability, or tighter control over settlement terms and processing economics.

What’s easy to miss is that these choices don’t just affect fees or tooling. They influence everything from payment approval rates to what options you have when a good customer still gets declined.

As we explored above, a revenue recovery engine like Paymend exists to convert eligible declined card transactions into settled revenue after the first attempt. Paymend retries eligible declined card transactions on its own infrastructure and applies next-best action logic while taking fraud liability. Paymend gives you a way to recover revenue from false declines without increasing fraud exposure, changing checkout, or adding customer friction.

If you want to see what you’re leaving on the table and what you can safely recover, contact Paymend today.